HMA Insights: Your source for healthcare news, ideas and analysis.

HMA Insights – including our new podcast – puts the vast depth of HMA’s expertise at your fingertips, helping you stay informed about the latest healthcare trends and topics. Below, you can easily search based on your topic of interest to find useful information from our podcast, blogs, webinars, case studies, reports and more.

Join us on Monday, March 6, 2023, at the Fairmont Chicago, Millennium Park, for “Healthcare Quality Conference: A Deep Dive on What’s Next for Providers, Payers, and Policymakers,” where Lee Fleisher, MD, chief medical officer and director of CMS’ Center for Clinical Standards and Quality, will deliver the keynote titled A Vision for Healthcare Quality: How Policy Can Drive Improved Outcomes.

HMA’s first annual quality conference will provide organizations the opportunity to “Focus on Quality to Improve Patients’ Lives.” Attendees will hear from industry leaders and policy makers about evolving health care quality initiatives and participate in substantive workshops where they will learn about and discuss solutions that are using quality frameworks to create a more equitable health system.

In addition to Fleisher, featured speakers will executives from ANCOR, CareOregon, Commonwealth Care Alliance, Council on Quality and Leadership, Intermountain Healthcare, NCQA, Reema Health, Kaiser Permanente, United Hospital Fund, and others.

Working sessions will provide expert-led discussions about how quality is driving federal and state policy, behavioral health integration, approaches to improving equity and measuring the social determinants of health, integration of disability support services, stronger Medicaid core measures, strategies for Medicare Star Ratings, value-based payments, and digital measures and measurement tools. Speakers will provide case studies and innovative approaches to ensuring quality efforts result in lasting improvements in health outcomes.

“What’s different about this conference is that participants will engage in working sessions that provide healthcare executives tools and models for directly impacting quality at their organizations,” said Carl Mercurio, Principal and Publisher, HMA Information Services.

View the Full Agenda

Early Bird registration ends January 30. Visit the conference website for complete details. Group rates and sponsorships are available.

As respiratory syncytial virus (RSV), a seasonal pathogen in young children is challenging the national health care system as part of an unprecedented “tripledemic” with COVID-19 and flu this winter, HMA authors weigh in on potential coverage pathways for new monoclonal antibody (mAb) preventive therapies for RSV and their implications for access.

The Vaccines for Children (VFC) program is a proven vehicle for ensuring comprehensive coverage of immunizations based on recommendations from the Advisory Committee on Immunization Practices (ACIP). An ACIP workgroup is actively discussing potential recommendations for immunization with RSV mAbs.

In the recent Health Affairs Forefront article, “Coverage By Vaccines For Children Program Is Critical For RSV Therapy Access,” HMA authors Helen DuPlessis, MD, FAAP, Diana Rodin, and Matt Wimmer explore the implications of ACIP recommendations, Medicaid coverage pathways, and children’s access to the new therapies.

This week, our In Focus section reviews changes to Medicaid’s COVID-19 Public Health Emergency (PHE) unwinding. People enrolled in the Medicaid program have been continuously enrolled for almost three years, but that situation is about to change. In December 2022, Congress passed, and the President signed into law a massive compromise bill to fund the government. It includes an important change to Medicaid’s continuous enrollment policy, which has been in effect since the early days of the COVID-19 PHE in March 2020.

Congress passed the Families First Coronavirus Relief Act (FFCRA) in March 2020. This legislation has allowed states to receive a 6.2 percentage point increase in their federal matching rate for Medicaid. As a condition for receiving the enhanced funding, states have been prohibited from disenrolling individuals who were otherwise determined ineligible for Medicaid. As a result, nearly 20 million more people are now enrolled in the Medicaid program.

The 2023 spending bill severs the link between the COVID-19 PHE declaration, the continuous enrollment requirement, and the higher federal match rate. The new law:

Ends the Medicaid continuous coverage policy on March 31, 2023, even if the PHE declaration remains in effect. States may begin issuing terminations of ineligible individuals as early as February 1, with an effective date of April 1.

Phases down the 6.2 percentage point increase in the federal matching rate rather than ending it abruptly at the end of the PHE as required under the FFCRA. Specifically, the increase will drop to 5 percentage points in April−June 2023, 2.5 percentage points in July−September 2023, and 1.5 percentage points in October−December 2023.

Does not end the PHE or other flexibilities linked to the PHE.

Congress also added new parameters and reporting requirements for states as they resume annual eligibility renewals with coverage cancellation for individuals who no longer qualify. These requirements are in addition to data the Centers for Medicare & Medicaid Services (CMS) previously directed states to report. For example:

States must maintain up-to-date enrollee contact information for individuals who will undergo an eligibility redetermination.

States cannot disenroll individuals based only on returned mail.

Prior to disenrolling an individual, the state must make a “good faith effort” to contact the person using more than one communication mode.

States must submit to CMS “on a timely basis” a report explaining their eligibility redetermination activities.

States must submit data related to individuals whose eligibility information was transferred between Medicaid and the Marketplace, with some exceptions for states that have integrated Medicaid and Marketplace eligibility systems and those that use the Federally Facilitated Marketplace.

Beyond the “Delinking”

The new law includes other important eligibility-related policies that may affect state and stakeholder planning for what is often referred to as the “unwinding” of continuous enrollment. Notably, the state Medicaid and CHIP programs will now be required to provide 12 months of continuous coverage for children. A total of 24 states already have adopted the 12-month continuous eligibility option for all children enrolled in Medicaid. While the new requirement will not take effect until January 1, 2024, additional states could adopt this option as they resume normal eligibility operations.

In addition, the new law makes permanent the option for states to extend Medicaid postpartum coverage to 12 months, up from 60 days. The one-year postpartum coverage option initially was approved in the American Rescue Plan but for a limited period of five years. Making the option permanent provides more certainty for states. Nearly two-thirds of states have already implemented or are planning to implement the 12-month postpartum coverage extension.

What Happens Next?

The definitive end date for the continuous enrollment policy sets in motion certain federal and state actions and the process for unwinding. On January 5, 2023, CMS published its first guidance to states on processes related to the new unwinding date. The agency is developing additional guidance and will use other communication tools to provide states with greater clarity on the new statutory reporting, matching rate, and federal agency expectations and oversight.

State plans: All states must submit unwinding plans to CMS by February 15; however, February 1 is the deadline for states that intend to begin renewals in February. These proposals must provide details regarding unwinding strategies, the timeline for starting enrollee renewals, and the pace of ongoing renewal processes. The specific end date for the continuous enrollment policy is driving more states to review and finalize their initiatives and engage with stakeholders.

Impact on health plans and providers: The unwinding process will create important decision points and considerations for Medicaid health plans and providers that have members and patients whom the unwinding process may affect in the next 12-18 months. The law’s requirements reinforce the imperative for states, Medicaid health plans, providers, and other partners to renew efforts to confirm enrollee contact information. The unwinding all will create new considerations for Medicaid health plans with respect to enrollee support, case mix, and rate setting issues.

State budgets and legislation: Many states will kick off their legislative sessions this month. The unwinding process—especially the phase-out of higher federal funding—has important implications for state budgets. State legislatures also may address the new continuous eligibility requirements for children and the permanent option for 12 months of postpartum coverage. As a result, Medicaid will likely remain a top priority during upcoming legislative sessions.

Federal oversight and enforcement: The law’s enhanced reporting provision is intended to provide safeguards to ensure eligible individuals remain enrolled in Medicaid. The reporting also focuses on data related to identifying and directing individuals likely to be eligible for the Marketplace program. Although CMS must publicly report these data, the agency has offered no specific timeline for posting the information. Notably CMS has oversight tools and may impose financial penalties on states that are noncompliant with the unwinding requirements.

Forthcoming federal guidance will confirm the parameters for state unwinding actions, CMS’s plans for oversight of state work, and how these efforts affect current Medicaid enrollees. Medicaid partners should closely monitor state level actions, including announcement of state unwinding plans and opportunities for collaboration. Earlier blogs describe the strategies and actions HMA is working with states and partners to undertake as they prepare for this significant change in Medicaid eligibility policies.

Please contact HMA experts below for more information.

The holiday season is grounded in gratitude. At HMA, we are grateful for successful partnerships that have fueled change to improve lives.

We are proud to be trusted advisors to our clients and partners. Their success is our success. In 2022 our clients and partners made significant strides tackling the biggest healthcare challenges, seizing opportunities for growth and innovation, and shaping the healthcare landscape in a way that improves the health and wellness of individuals and communities.

HMA partnered with the Colorado Department of Human Services to support the planning and implementation of a new Behavioral Health Administration (BHA). HMA provided technical research and extensive stakeholder engagement, drafted models for forming and implementing the BHA, employed an extensive change management approach, and created a detailed implementation plan with ongoing support. Today the BHA is a cabinet member-led agency that collaborates across agencies and sectors to drive a comprehensive and coordinated strategic approach to behavioral health.

Wakely Consulting Group, an HMA Company, was engaged to support the launch of a Medicare Advantage (MA) joint venture partnership between a health plan and a provider system. Wakely was responsible for preparing and certifying MA and Medicare Part D (PD) bids, a highly complex, exacting, and iterative effort. The Wakely team quickly became a trusted advisor and go-to resource for the joint venture decision makers. The joint venture has driven significant market growth over its initial years, fueled by a competitive benefit package determined by the client product team.

In 2021 Indiana Governor Eric Holcomb appointed a 15-member commission to assess Indiana’s public health system and make recommendations for improvements. The Indiana Department of Health (IDOH) engaged HMA to provide extensive project management and support for six workstreams. HMA prepared a draft report summarizing public input as well as research findings and recommendations. The commission’s final report will form the basis of proposed 2023 legislation, including proposals to substantially increase public health service and funding across the state.

In early 2022 HMA and Wakely Consulting Group, an HMA Company, assisted multiple clients with their applications to participate in the new CMS ACO REACH model. The purpose of this model is to improve quality of care for Medicare beneficiaries through better care coordination and increased engagement between providers and patients including those who are underserved. The team tailored their support depending on each client’s needs. The application selection process was highly competitive. Of the 271 applications received, CMS accepted just under 50 percent. Notably, nine out of the 10 organizations HMA and Wakely supported were accepted into the model.

HMA, and subsidiaries The Moran Company and Leavitt Partners, were selected by a large pharmaceutical manufacturer to analyze the current pipeline of innovative therapies, examine reimbursement policies to assess long-term compatibility with the adoption of innovative therapies and novel delivery mechanisms, and make policy recommendations to address any challenges identified through the process. The project equipped the client with a holistic understanding of future potential impacts and actions to address challenges in a detailed pipeline analysis of innovative therapies.

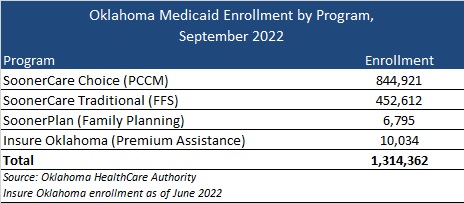

This week, our In Focus reviews the Oklahoma Medicaid managed care SoonerSelect Program request for proposals (RFP) and the SoonerSelect Children’s Specialty Program RFP released by the Oklahoma Health Care Authority (OHCA) on November 10, 2022.

Background

Oklahoma currently does not have a fully capitated, risk-based Medicaid managed care program. The majority of the state’s 1.3 million Medicaid members are in SoonerCare Choice, a Primary Care Case Management (PCCM) program in which each member has a medical home. Other programs include SoonerCare Traditional (Medicaid fee-for-service), SoonerPlan (a limited benefit family planning program), and Insure Oklahoma (a premium assistance program for low-income people whose employers offer health insurance).

Prior efforts to transition to Medicaid managed care have encountered roadblocks, starting in 2017 with a failed attempt to move aged, blind, and disabled members to managed care.

More recently, in June 2021, the Oklahoma Supreme Court struck down a planned transition of the state’s traditional Medicaid program to managed care, ruling that the Oklahoma Health Care Authority does not have the authority to implement the program without legislative approval.

Contracts had been awarded to Blue Cross Blue Shield of Oklahoma, Humana, Centene/Oklahoma Complete Health, and UnitedHealthcare. Centene/Oklahoma Complete Health also won an award for the SoonerSelect Children’s Specialty Program.

In May 2022, Governor Kevin Stitt signed a new Oklahoma law to implement Medicaid managed care by October 1, 2023.

SoonerSelect RFP

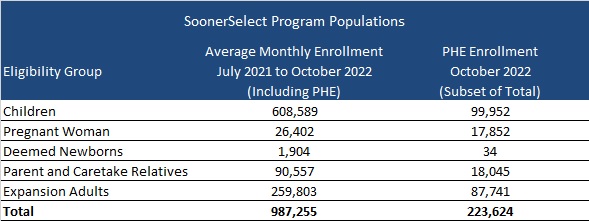

Oklahoma will award contracts to at least three entities to provide medical, behavioral, and pharmacy coverage to nearly one million eligible children, pregnant women, newborns, parents and caretake relatives, and the expansion population. However, enrollment in these populations is expected to drop following the end of the public health emergency (PHE).

At least one of the contracts may be awarded to a provider-led entity (PLE). PLEs would need to provide proof that a majority of their ownership is held by Oklahoma Medicaid providers or the majority of the governing body is composed of individuals who have experience serving Medicaid members and are licensed providers. PLEs would also be able to bid on urban regions if the PLE agrees to develop statewide readiness within a timeframe set by the OHCA. If no PLEs meet OHCA standards, Oklahoma can choose not to award a PLE.

Goals of the program will include:

Improve health outcomes for Medicaid members and the state as a whole

Ensure budget predictability through shared risk and accountability

Ensure access to care, quality measures, and member satisfaction

Ensure efficient and cost-effective administrative systems and structures

Ensure a sustainable delivery system that is a provider-led effort and that is operated and managed by providers to the maximum extent possible.

Timeline

Proposals will be due on February 8, 2023, and contract implementation is scheduled for October 1, 2023. The contract is expected to run through June 30, 2024, with five, one-year options.

Evaluation

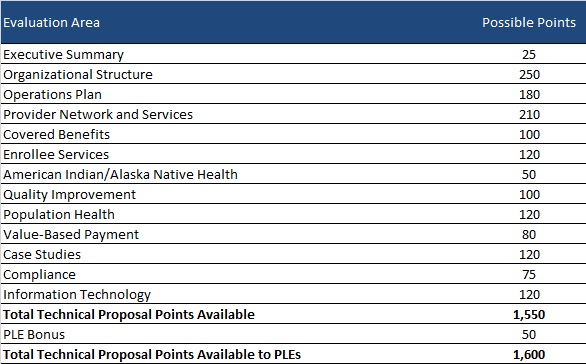

Bidder’s technical proposals will be scored out of a total 1550 points. OHCA will award PLEs an additional 50 points for qualifying, bringing the total up to 1600 points. OHCA may also choose to conduct oral presentations for an extra total of 50 points.

SoonerSelect Children’s Specialty Program RFP

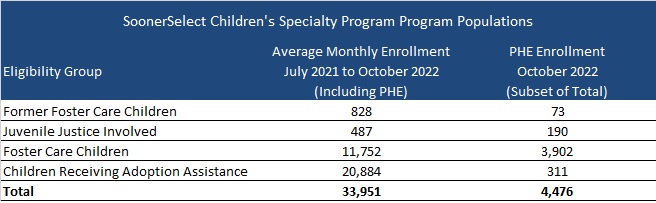

Oklahoma will select one of the awarded SoonerSelect plans for a separate statewide contract to provide comprehensive integrated health coverage to foster children, former foster children up to 25 years of age, juvenile justice-involved children, and children receiving adoption assistance. Contract terms will be the same as the main SoonSelect procurement, running from October 1, 2023, through June 30, 2024, with five one-year renewal options.

While the current federal COVID-19 Public Health Emergency (PHE) declaration could be in place through the winter months, HMA’s team of experts see many reasons to put the PHE’s Medicaid unwinding planning at the top of your list now.

Without an extension, the PHE declaration will expire on January 11, 2023. U.S. Department of Health and Human Services (HHS) officials pledged to provide 60-days’ notice before ending the PHE. As a result, since HHS did not announce an extension by November 12, we can assume that HHS Secretary Xavier Becerra will extend the PHE beyond January.

However, congressional leaders are again considering proposals that would impact the PHE’s Medicaid policies. Such a change could advance during the lame duck session of Congress. For a variety of reasons, lawmakers could seek a statutory change that would de-link Medicaid’s continuous enrollment requirement, the 6.2 percentage point increase in the federal Medicaid match, and other Medicaid maintenance of effort policies from the PHE declaration. Congress could set a specific date for ending these Medicaid policies. Doing so would provide more certainty for planning for the end of the continuous Medicaid enrollment policy and its downstream implications for health insurance programs.

What can Medicaid agencies, health plans, providers and other stakeholders do now?

The transition from Medicaid’s continuous enrollment requirement to normal eligibility operations involves a myriad of policy decisions and operational changes that will impact enrollees. In turn, the end of Medicaid’s continuous coverage policy will also have great bearing on the business and operational strategies of managed care plans, providers and other stakeholders participating in the Medicaid and Marketplace programs.

HMA’s experts are working with state agencies, health plans, hospitals and health systems, and other stakeholders to identify options and workable solutions to prepare for these major changes. This work touches policy, organizational workstreams, systems, and payment. There are issues specific to Medicaid as well as the intersection with Marketplace, the Supplemental Nutrition Program (SNAP), and other public programs.

Combining our collective on-the-ground experience in states with our federal policy insights, experts from across the HMA family of companies list below themes and immediate actions stakeholders can consider. These action steps are focused on ensuring states, managed care plans, providers and other stakeholders are prepared to immediately respond to the end of the Medicaid continuous enrollment policy and work with individuals to provide information and other support they may need to stay enrolled in a coverage program.

Monitor and prepare for federal activities, particularly during the lame duck session of Congress and into 2023. Healthcare policies are likely to feature prominently in Congress’ lame duck session in November and December. Decoupling the Medicaid continuous enrollment and enhanced Federal Medical Assistance Percentage (FMAP) policies from the PHE is one issue under consideration. Any statutory changes to these policies may also include new requirements for the unwinding process. Stakeholders will want to closely monitor these discussions. If Congress sets a statutory end date for the PHE’s Medicaid eligibility policies, this will provide the certainty needed for states to finalize PHE unwinding action plans with target dates for resuming normal eligibility operations. Notably, this may also drive conversations during states’ 2023 legislative sessions.

Stay informed about state-specific landscapes. With statewide elections largely decided and expectations for a PHE end date sometime in the first part of 2023, now is the time for stakeholders to revisit when and how to engage with state Medicaid and other state agencies to support Medicaid eligibility unwinding plans. Stakeholders will want to solidify strategies and timing for engaging with states as unwinding plans are further solidified and eventually implemented. Stakeholders can also monitor changes to states’ eligibility and enrollment rules – including initiatives designed to simplify eligibility rules, enhance eligibility and enrollment systems, and adjust managed care rate setting policies, among others. Many states are utilizing the temporary federal Medicaid flexibilities to alleviate the significant eligibility unwinding workload. Federal agencies also continue to regularly publish new information for states and stakeholders to consider. Some states are implementing policies designed to improve the transition from Medicaid to Marketplace. Understanding the implications of such policies will help stakeholders anticipate how ending Medicaid’s continuous coverage requirement will directly affect them.

Refresh strategies and messaging for outreach and assistance. While the PHE end date remains in flux, state plans for ending the Medicaid continuous coverage policy are still evolving. States are refining their beneficiary communication plans and may be developing updated guidance for stakeholders. Health plans, providers, and other stakeholders should align their messaging and outreach work accordingly and continue to build partnerships in communities across the state. However, outreach alone will not be enough to reach all Medicaid enrollees. Many will need assistance in understanding and complying with changes that come with the end of the continuous enrollment policy. For example, stakeholder-provided redetermination assistance will be key to minimizing the number of enrollees who lose coverage for failure to complete the redetermination process and state requirements for stakeholder assistance will vary state by state.

Update projected impact of enrollee transitions between Medicaid and Marketplace programs. For states and stakeholders, especially health plans, it is time to update projections about 2023 Medicaid and Marketplace enrollment. This may also require new analysis and strategies to address the changing population acuity and resulting impact on capitation revenue. For healthcare providers, health systems, and other healthcare facilities, the end of the Medicaid continuous enrollment policy is expected to drive significant changes in payer mix, and it could reduce revenue as well as impact qualifications for special payment programs, the 340B program, among others. Understanding these dynamics can help with budgeting and implementation of specific patient outreach and support strategies.

5. Develop strategies to translate experiences from Medicaid to Marketplace. Medicaid agencies, managed care plans, and providers have gained valuable insights about the needs of individuals who have remained continuously enrolled in Medicaid during the COVID-19 PHE. This is particularly true for Medicaid enrollees diagnosed with a mental illness, substance use disorder, or both. Medicaid providers and health plans have gained valuable insight on effective clinical care models, whole person care, partnerships with community-based organizations and reimbursement strategies that can better meet the needs of complex populations. Providers and plans can utilize these experiences to better support the millions of individuals who are expected to become eligible for Marketplace coverage after Medicaid’s continuous enrollment policy ends.

The HMA team continues to monitor the dynamic state and federal policy landscapes, including state planning documents and new federal guidance and informational tools. We have the ability to support stakeholders to prepare for the end of PHE and to support state and communities by modeling projected enrollment and payer mix changes across health coverage categories. Stakeholders should be using this time to address gaps in their plans for PHE unwinding and continue to identify and evaluate new options that may emerge to support beneficiaries in retaining health coverage.

This week, our In Focus section reviews highlights and shares key takeaways from the 22nd annual Medicaid Budget Survey conducted by The Kaiser Family Foundation (KFF) and Health Management Associates (HMA). Survey results were released on October 25, 2022, in two new reports: How the Pandemic Continues to Shape Medicaid Priorities: Results from an Annual Medicaid Budget Survey for State Fiscal Years 2022 and 2023 and Medicaid Enrollment & Spending Growth: FY 2022 & 2023. The report was prepared by Elizabeth Hinton, Madeline Guth, Jada Raphael, Sweta Haldar, and Robin Rudowitz from the Kaiser Family Foundation and by Kathleen Gifford, Aimee Lashbrook, and Matt Wimmer from HMA; and Mike Nardone. The survey was conducted in collaboration with the National Association of Medicaid Directors (NAMD).

This survey reports on policies in place or planned for FY 2022 and FY 2023, including state experiences with policies adopted in response to the COVID-19 pandemic. The conclusions are based on information provided by the nation’s state Medicaid Directors.

Key Report Highlights

In the following sections, we highlight a few of the major findings from the reports. This is a fraction of what is covered in the 50-state survey reports, which include significant detail and findings on policy changes and initiatives related to delivery systems, health equity, benefits, telehealth, provider rates and taxes, and pharmacy. The reports also look at the opportunities, challenges, and priorities facing Medicaid programs.

Medicaid Enrollment and Spending Growth

The COVID-19 pandemic created significant implications for Medicaid. During this time, Medicaid enrollment has reached record highs due to the Families First Coronavirus Response Act (FFCRA), enacted in March 2020, which authorized a 6.2 percentage point increase in the federal match rate, or Federal Medical Assistance Percentage (FMAP), retroactive to January 1, 2020, and until the Public Health Emergency (PHE) ends. The increase was available to states that meet certain “maintenance of eligibility” (MOE) requirements. Since the survey, the PHE was extended to mid-January 2023, somewhat delaying the anticipated effects described in survey.

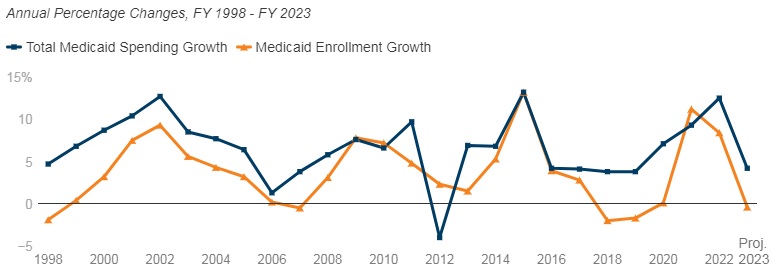

Medicaid enrollment growth slowed to 8.4 percent in FY 2022, after a sharp increase in FY 2021 (11.2 percent). Almost all responding states reported that the MOE continuous enrollment requirement was the most significant factor driving FY 2022 enrollment growth. Responding states expect Medicaid enrollment growth to decline (-0.4 percent) in FY 2023, based largely on the assumption that the PHE and the related MOE requirements would end by mid-FY 2023. States anticipate larger declines as Medicaid redeterminations and renewals resume.

In FY 2022, total Medicaid spending is expected to reach a peak growth of 12.5 percent, with enrollment growth as the primary driver. For FY 2023, total spending growth is expected to slow to 4.2 percent, assuming slower enrollment growth after the unwinding of the PHE. State Medicaid spending grew by 9.9 percent in FY 2022 and is projected to increase by 16.3 percent in FY 2023 once enhanced federal fiscal relief expires. If the PHE is extended, state spending increases and enrollment decreases that states anticipated for FY 2023 could occur later.

Figure 1 – Percent Change in Medicaid Spending and Enrollment, FY 1998-23

SOURCE: FY 2022-2023 spending data and FY 2023 enrollment data are derived from the KFF survey of Medicaid officials in 50 states and DC conducted by Health Management Associates, October 2022. 49 states submitted survey responses by Oct. 2022; state response rates varied across questions. Historic data reflects growth across all 50 states and DC and comes from various sources.

Delivery Systems

Capitated managed care remains the predominant delivery system for Medicaid in most states. Forty-six states operated some form of Medicaid managed care (managed care organizations (MCOs) and/or primary care case management (PCCM)). Forty-one states contracted with risk-based MCOs. Of these, only Colorado and Nevada did not offer MCOs statewide. Only five states – Alaska, Connecticut, Maine, Vermont, and Wyoming – lacked a comprehensive Medicaid managed care model.

Thirty-four states, including Distrct of Columbia, operate MCOs only, five states operate PCCM programs only, and seven states operate both MCOs and a PCCM program.

Twenty-seven states contracted with one or more PHPs to provide Medicaid benefits, including behavioral health care, dental care, vision care, non-emergency medical transportation (NEMT), and long-term services and supports (LTSS).

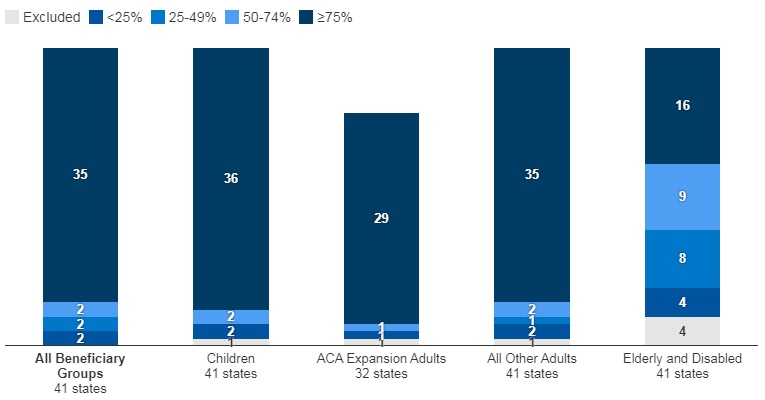

Of the forty-one states that contracted with MCOs, 35 reported that 75 percent or more of their Medicaid beneficiaries were enrolled in MCOs as of July 1, 2022.

Figure 2 – MCO Managed Care Penetration Rates for Select Groups of Medicaid Beneficiaries as of July 1, 2022

SOURCE: KFF survey of Medicaid officials in 50 states and DC conducted by HMA, October 2022.

Medicaid Managed Care and Delivery System Changes

California, Missouri, Nevada, New Jersey, and New York reported expanding mandatory MCO enrollment for targeted populations.

Missouri and Ohio reported introducing specialized managed care programs for children with complex needs.

California, Nevada, and Tennessee indicated that they were carving in certain long-term services and supports (LTSS) into their managed care programs.

California and Ohio reported carving out pharmacy services in FY 2022 or FY 2023, respectively. The District of Columbia carved out emergency medical transportation from its MCO contracts in FY 2022.

Maine, North Carolina, Oregon, and Washington reported changes to their PCCM programs.

Virginia plans to implement Cardinal Care in FY 2023, merging the state’s two existing managed care programs: Medallion 4.0 (serving children, pregnant individuals, and adults) and Commonwealth Coordinated Care Plus (CCC Plus) (serving seniors, children and adults with disabilities, and individuals who require LTSS).

Forty-one states reported at least one specified delivery system and payment reform initiative (e.g. Patient-Centered Medical Home (PCMH), ACA Health Homes, Accountable Care Organization (ACO), Episode of Care Initiatives, All-Payer Claims Database (APCD)).

Health Equity

Twenty-five states reported using at least one specified strategy to improve race, ethnicity, and language (REL) data completeness. Of the 45 responding states, 16 states reported requiring MCOs and other applicable contractors to collect REL data, 12 states reported that eligibility, renewal materials, and/or applications explain how REL data will be used and/or why reporting these data are important, nine states reported linking Medicaid enrollment data with public health department vital records data, and eight states reported partnering with one or more health information exchanges (HIEs) to obtain additional REL data for Medicaid enrollees.

Twelve of 44 responding states reported at least one financial incentive tied to health equity in place in FY 2022. The vast majority of these incentives were in place in managed care arrangements (11 of 13). Within managed care arrangements, states most commonly reported linking or planning to link capitation withholds, pay for performance incentives, and/or state-directed provider payments to health equity-related quality measures. Only two states (Connecticut and Minnesota), reported a FFS financial incentive in FY 2022. Five additional states report plans to implement financial incentives linked to health equity in FY 2023.

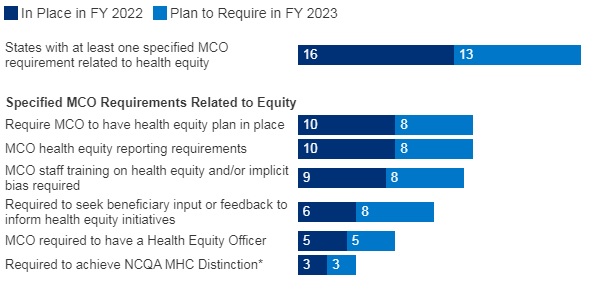

Sixteen of 37 responding MCO states reported at least one specified health equity MCO requirement in place in FY 2022. The number of MCO states with at least one specified health equity MCO requirement in place is expected to grow significantly in FY 2023, from 16 to 25 states. Examples of MCO requirements to address health equity include having a health equity plan, designating a Health Equity Officer, and staff training on health equity and/or implicit bias.

Figure 3 – MCO Requirements to Address Health Equity, FYs 2022-23

SOURCE: KFF survey of Medicaid officials conducted by HMA, October 2022; n=37 states.

Benefits

Thirty-three states reported new or enhanced benefits in FY 2022 and 34 states are adding or enhancing benefits in FY 2023. Two states reported benefit cuts or limitations in FY 2022 and no states reported cuts or limitations in FY 2023.

Figure 4 – Select Categories of Benefit Enhancements or Additions, FYs 2022-23

SOURCE: KFF survey of Medicaid officials conducted by HMA, October 2022; Arkansas and Georgia did not respond.

Behavioral Health Services. States reported service expansions across the behavioral health care continuum, including institutional, intensive, outpatient, home and community-based, and crisis services. States reported addressing SUD outcomes, including coverage of opioid treatment programs, peer supports, and enhanced care management. At least ten states are expanding coverage of crisis services, which aim to connect Medicaid enrollees experiencing behavioral health crises to appropriate community-based care, including mobile crisis response services and crisis stabilization centers.

Pregnancy and Postpartum Services. In April 2022, a temporary option under ARPA to extend Medicaid postpartum coverage from 60 days to 12 months took effect. In addition to the states that took advantage of this eligibility change, some states are enhancing coverage of pregnancy and post-partum services. Nine states (California, District of Columbia, Illinois, Maryland, Michigan, New Mexico, Nevada, Rhode Island, and Virginia) are adding coverage of services provided by doulas and seven states (Alabama, Delaware, Illinois, Maryland, Ohio, Oregon, and Vermont) are investing in the implementation or expansion of home visiting programs.

Preventive Services. Sixteen states reported expansions of preventive care in FY 2022 or FY 2023. For example, seven states are expanding services to prevent and/or manage diabetes, such as continuous glucose monitoring. Other reported preventive benefit enhancements relate to asthma services, vaccinations, and genetic testing and/or counseling.

Services Targeting Social Determinants of Health. Many states reported new and expanded benefits targeting social determinants of health. Twelve states reported new or expanded housing-related supports, as well as other services and programs tailored for individuals experiencing homelessness or at risk of being homeless.

Dental Services. Nine states are adding comprehensive adult dental coverage, while additional states report expanding specific dental services for adults.

Telehealth

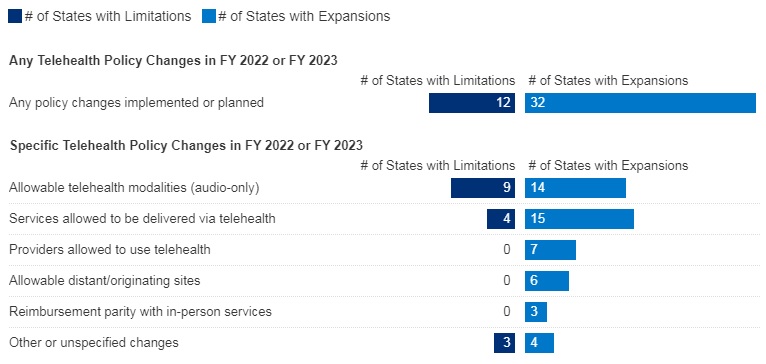

Most states have or plan to adopt permanent Medicaid FFS telehealth expansions that will remain in place even after the pandemic, though some are considering guardrails on such policies. Nearly all responding states that contract MCOs reported that changes to FFS telehealth policies would also apply to MCOs.

Figure 5 – Changes to FFS Medicaid Telehealth Policy, FY 2022 or FY 2023

SOURCE: KFF survey of Medicaid officials conducted by HMA, October 2022; n=48 states.

Nearly all responding states added or expanded audio-only telehealth coverage in Medicaid in response to the COVID-19 pandemic. Twenty-eight states reported that they newly added audio-only coverage while 19 states expanded existing coverage. Nearly all states reported audio-only coverage of mental health and substance use disorder (SUD) services. States least frequently reported audio-only coverage of home and community-based services (HCBS) and dental services. Two states (Mississippi and Wyoming) reported no coverage of audio-only telehealth for the services in question.

Telehealth utilization by Medicaid enrollees has been high during the pandemic but has decreased and/or leveled off more recently. States noted that telehealth utilization trends over time correspond to COVID-19 outbreaks, with higher utilization during COVID-19 surges and lower utilization when case counts are lower. In general, states reported that telehealth utilization was projected to continue at higher levels than before the pandemic, at least for some service categories.

Thirty-seven states (out of 47 responding) reported that behavioral health services were among those with the highest utilization. Additionally, a majority of states reported high utilization of evaluation and management (E/M) services and/or other physician/qualified health care professional office/outpatient services, including primary care.

States reported ACA expansion adults as one of the groups most likely to use telehealth (about one-third of responding states), followed by children and individuals with disabilities (each identified by about one-sixth of responding states).

Concerns regarding services delivered via telehealth included the quality of diagnoses, whether audio-only telehealth may be less effective, and inadequate access.

Key issues that may influence future Medicaid telehealth policy decisions include analysis of data, state legislation and federal guidance, and cost concerns.

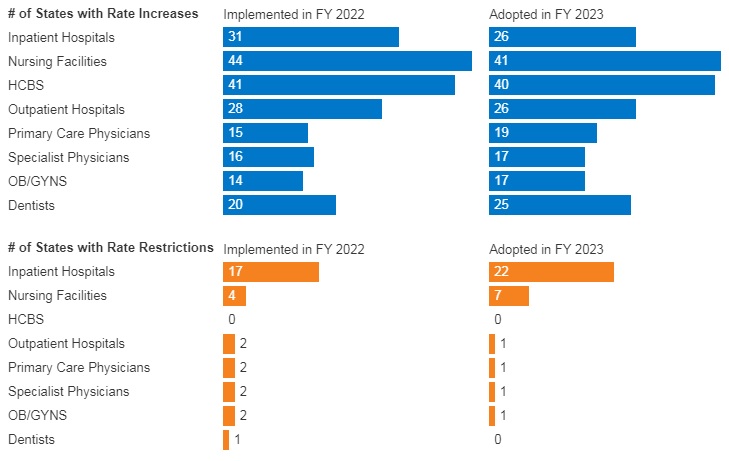

Provider Rates and Taxes

In FY 2022, all 49 responding states reported implementing rate increases for at least one category of provider and 19 states reported implementing rate restrictions. In FY 2023, 48 states reported at least one planned rate increase and the number of states planning to restrict rates increased to 25 states.

States reported rate increases for nursing facilities and home and community-based services (HCBS) providers more often than other provider categories. The survey also found an increased focus on dental rates with about half of reporting states (20 in FY 2022 and 25 in FY 2023) reporting implementing or plans to implement a dental rate increase

Figure 6 – FFS Provider Rate Changes Implemented in FY 2022 and Adopted for FY 2023

SOURCE: KFF survey of Medicaid officials in 50 states and DC conducted by HMA, October 2022.

States continue to rely on provider taxes and fees to fund a portion of the non-federal share of Medicaid costs. All states but Alaska have at least one provider tax or fee in place. Thirty-eight states had three or more provider taxes in place in FY 2022 and eight other states had two provider taxes in place.

The most common Medicaid provider taxes in place in FY 2022 were taxes on nursing facilities (46 states), followed by taxes on hospitals (44 states), intermediate care facilities for individuals with intellectual disabilities (33 states), and MCOs (18 states).

Three states (Alabama, Mississippi, and Wyoming) reported plans to add new ambulance taxes in FY 2023.

Pharmacy

Most states that contract with MCOs report that the pharmacy benefit is carved into managed care (34 out of 41 states that contract with MCOs). Six states (California, Missouri, North Dakota, Tennessee, Wisconsin, and West Virginia) report that pharmacy benefits are carved out of MCO contracts as of July 1, 2022. California was the latest to carve out pharmacy benefits as of January 1, 2022. Two states (New York and Ohio) report plans to carve out pharmacy from MCO contracts in state FY 2023 or later.

In FY 2022, Kentucky began contracting with a single PBM for the managed care population. Louisiana and Mississippi report that they will require MCOs to contract with a single PBM designated by the state in FY 2023 and FY 2024, respectively.

Seven states (Alabama, Arizona, Colorado, Massachusetts, Michigan, Oklahoma, and Washington) have value-based arrangements (VBAs) in place with one or more drug manufacturers.

More than half of responding states reported newly implementing or expanding at least one initiative to contain prescription drug costs in FY 2022 or FY 2023.

Six states (Florida, Kentucky, Massachusetts, Maryland, Nebraska, Nevada) reported recently implemented or planned policies to prohibit spread pricing or require pass through pricing in MCO contracts with PBMs.

Key Opportunities, Challenges, and Priorities in FY 2023 and Beyond

When asked to identify the top challenges for FY 2023 and beyond, Medicaid directors listed the following:

The unwinding of PHE emergency measures and the resumption of redeterminations.

Expiration of emergency authorities.

Lasting focus on COVID-19, including vaccinations, long-COVID, decreased utilization of preventive care services, and future emergency preparedness.

Medicaid directors stated that future priorities shaped by COVID-19 include:

Health equity.

Specific populations and service categories, including behavioral health, long-term services and supports, and maternal and child health.

Health care workforce challenges.

Payment and delivery system initiatives and operations.

IT system modernization.

Social determinants of health.

Medicaid directors note that COVID-19 has presented both new opportunities and challenges and has also shifted and shaped ongoing Medicaid priorities.

The 22nd annual Medicaid Budget Survey conducted by The Kaiser Family Foundation (KFF) and Health Management Associates (HMA) was released on October 25, 2022, in the report: How the Pandemic Continues to Shape Medicaid Priorities: Results from an Annual Medicaid Budget Survey for State Fiscal Years 2022 and 2023.

The report was prepared by Kathleen Gifford, Aimee Lashbrook, and Matt Wimmer from HMA; Mike Nardone; and by Elizabeth Hinton, Madeline Guth, Jada Raphael, Sweta Haldar, and Robin Rudowitz from the Kaiser Family Foundation. The survey was conducted in collaboration with the National Association of Medicaid Directors (NAMD).